Background

At the Citi 2026 Global Property CEO Conference, we met in person with 41 US and global REIT management teams and toured residential, industrial, retail, and tower assets. The tone was noticeably more upbeat than recent conferences we have attended and even a step-change from NAREIT’s December conference in Dallas.

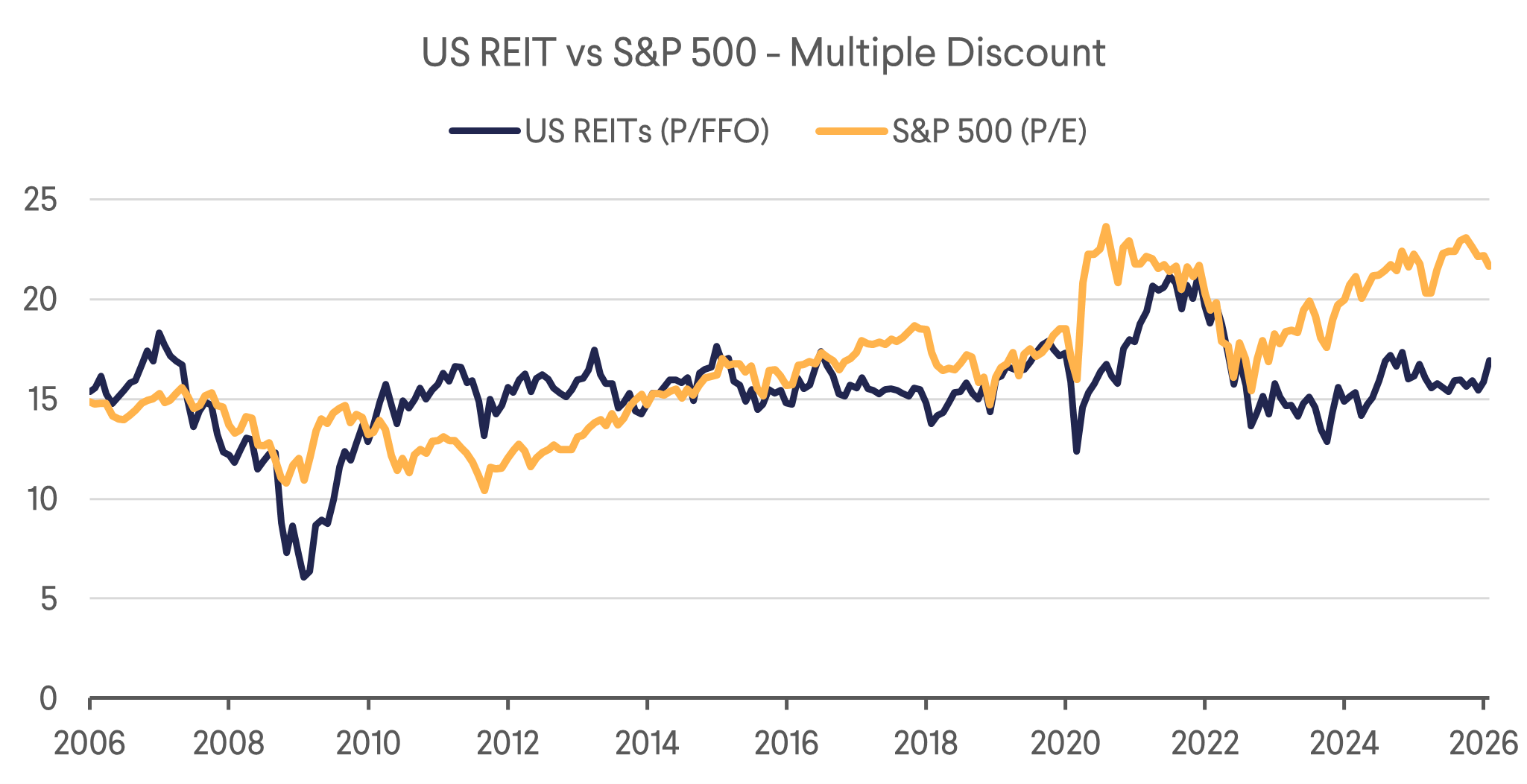

The sentiment shift is reflected in strong relative REIT performance YTD, with the sector up 8.2% versus down 1.3% for the S&P 500 and down 2.4% for the Nasdaq. Reasons for the shift include that REITs had reached historically wide relative valuation levels to equities as well as being universally underweight in asset allocation strategies, meaning it does not take much capital rotating out of other richly valued equities to have a positive effect on REITs. YTD REITs had also benefited from falling interest rates, with the 10 year Treasury briefly dipping below 4% the week before the conference.

It also looks like most REIT sectors fall into the so-called ‘HALO’ trade, where heavy-asset areas of the market with low obsolescence are viewed as less exposed to AI driven risks.

As we write this, the war in the Middle East war is only a week old, and it is very difficult to determine the ultimate effect this will have on markets. A quick resolution would have oil prices and rates dropping quickly back to previous levels while a prolonged and expanding conflict could imply an energy-led inflation shock with rates moving higher.

While geopolitical headlines dominated the news flow during the event, most of our discussions with management teams centered on AI, specifically how advances in AI could help or hurt different commercial real estate sectors. Despite the uncertainty, many companies continue to benefit from conservative balance sheets, improving access to capital, and improving supply demand dynamics which support rent growth and pricing power across several property types.

AI’s Impact on Real Estate – This Time is Different?

In every meeting and tour, investors asked some version of, “How will AI adoption impact your company and sector?” AI can already take on complex cognitive work, generate inspired content, and in some cases make decisions with very little human involvement. That has led to extreme predictions and headlines that AI will wipe out large parts of white-collar employment. Markets have reacted to those fears, shooting first and asking questions later.

However, as the famous Sir John Templeton quote reminds investors, the four most dangerous words are, “this time is different.” AI is unlike past tools in its ability to create and learn, but even the most disruptive technologies rarely lead to entirely permanent and broad job losses.

For example, the emergence of the internet wiped out travel agencies, the yellow pages, video rental stores, photo processing labs, print shops, and a long list of clerical roles that were built around paper, phone calls, and physical distribution. At the same time, it created e-commerce, cloud computing, digital advertising, online payments, cybersecurity, and millions of jobs that did not exist before. If history is a guide, AI will be disruptive, but it will also be creative. It will likely open the door to new business models, new types of demand, and new jobs that are hard to imagine today.

Depending on the specific sector, there are reasons to believe REITs and real estate will be net beneficiaries of AI. Real estate ultimately houses the economy, so if AI raises productivity, incomes, and living standards, REITs should benefit over time.

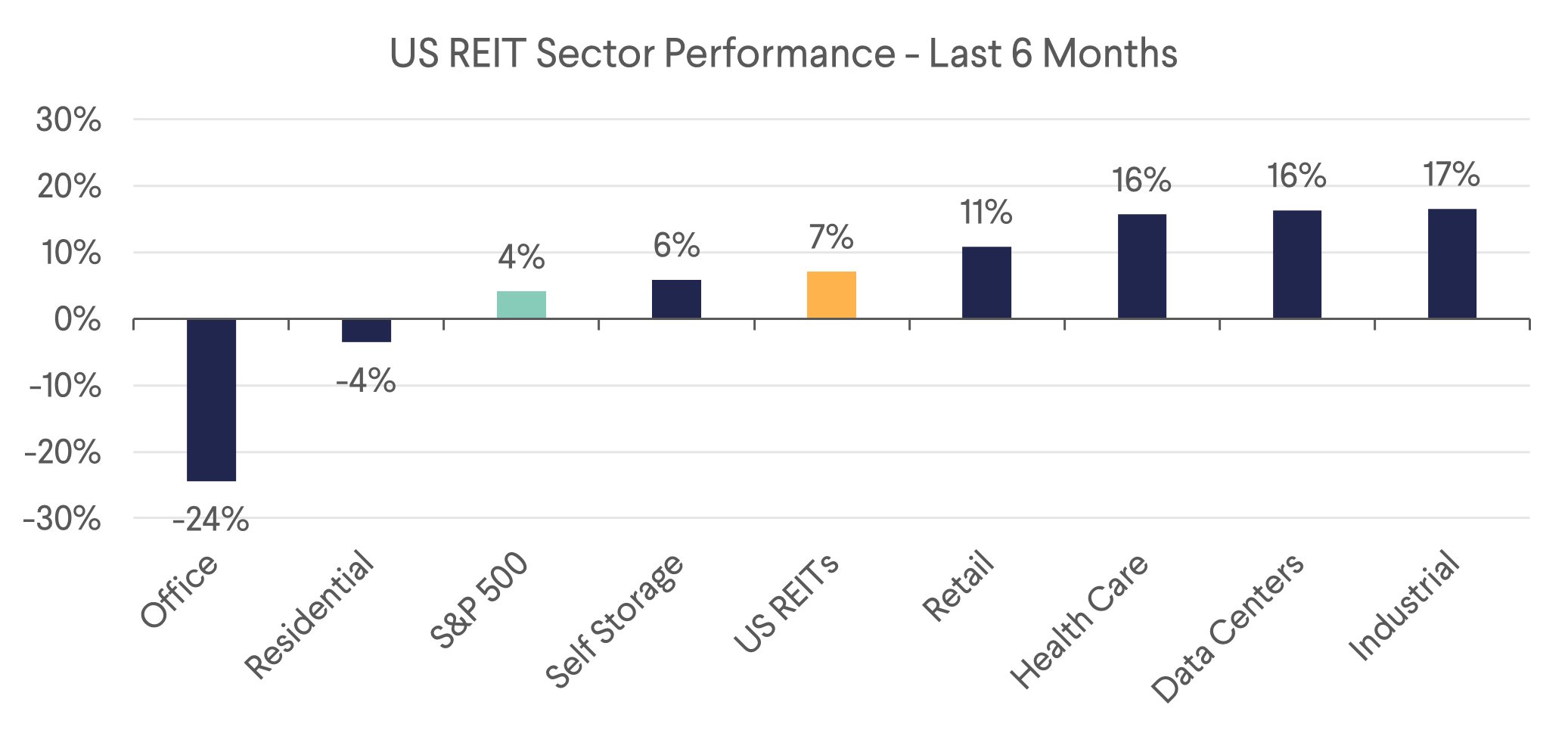

Over the past six months, investors have been fixated on the idea that AI could lead to widespread job losses. That fear has hit the REIT sectors most tied to white-collar employment, especially Office and Residential, which have seen the sharpest pullbacks. Meanwhile, areas of the market that don’t depend as directly on headcount such as Industrial, Healthcare, and Retail have held up well. Data Centers, which clearly benefit from AI investments, have also performed well.

Supply Fundamentals Improving

While fundamentals vary across geographies and subsectors, many CEOs expect KPIs to improve, supported by a constructive supply backdrop. Low supply is an important factor, but insufficient on its own to drive strong performance. An inflection in growth will also depend on other factors like a healthy economic environment, uncertainty around AI disruption, geopolitical risks, and the rate environment.

The Retail sector illustrates this well: supply remained depressed for many years, yet the sector still endured a prolonged period of weak returns. Growth inflection ultimately requires healthy demand for space from tenants.

In Retail, an extended period of low supply combined with a post-pandemic demand recovery drove steady occupancy improvements and a same-store NOI growth recovery. Both strip center and mall operators highlighted that new supply remains extremely low, typically below ~0.5% annually, with development largely limited to grocery-anchored centers tied to housing growth. High construction costs and long development timelines continue to constrain new projects.

Industrial and Self-Storage, by contrast, have faced elevated supply in recent years which, combined with weakening demand, drove rising vacancy rates and negative market rent growth in 2025. However, development completions are declining in both sectors and should help tighten market conditions as current vacancies are absorbed.

Sector Takeaways

Data Centers

Management from Equinix and Digital Realty highlighted continued strong demand for data center capacity, increasingly driven by AI workloads in addition to the existing growth trend in hyperscale cloud infrastructure. Hyperscalers continue to invest aggressively as competition remains focused on gaining scale and market share.

AI is becoming a significant driver of leasing activity. EQIX indicated that around 60% of its largest deals are AI-related, while Digital Realty noted growing competition for capacity between existing hyperscale customers and emerging AI companies.

EQIX highlighted that AI is progressively using more interconnect, one of their core strengths.

Power availability and infrastructure development timelines remain the primary constraints on supply, as energy permitting and grid connections become increasingly complex and time-consuming. Locations with power capacity are highly valued, sometimes even outweighing traditional location advantages. Overall, sector sentiment remains constructive, supported by strong leasing pipelines and expanding demand from AI-driven computing infrastructure.

Industrial and Storage

Industrial and self-storage are emerging from a period of weaker demand and elevated supply and are now on a gradual path toward recovery. While both sectors are benefiting from declining supply pressure, improvements in demand are currently more visible in industrial real estate. Leasing activity picked up in Q4 and has continued to improve year-to-date.

Tariff uncertainty in 2025 led to delayed leasing decisions. While global trade risks remain, tenants are increasingly willing to look through these uncertainties or can no longer postpone leasing decisions.

Los Angeles, which was one of the strongest markets a few years ago, continues to lag the broader recovery and has now reported negative absorption for twelve consecutive quarters. Views on the timing of a recovery differ among operators. Non-listed Link Logistics (owned by Blackstone) believes the market has stabilized and that conditions are no longer deteriorating. In contrast, SoCal-focused REIT Rexford issued cautious guidance for 2026. EastGroup, which focuses primarily on Sunbelt markets, currently sees stronger opportunities elsewhere and prefers to wait for clearer signs that Los Angeles is not facing structural demand challenges related to slower population growth and local political factors.

Self-storage demand remains largely necessity-driven, but housing turnover, a key demand driver, remains subdued resulting in continued negative same-store NOI outlooks for the current year. In this environment, operators are focusing primarily on capturing market share through marketing, pricing optimization, and customer acquisition strategies, rather than stimulating demand through price changes alone. Increasingly, operators are leveraging data analytics and AI-driven revenue management tools to improve pricing precision and marketing efficiency.

Retail

All retail REIT subsectors delivered strong post-Covid performance and continue to benefit from resilient consumer spending combined with extremely limited new supply, which remains among the lowest in the sector.

Retail REITs tend to focus on higher-income demographic areas, which has proven advantageous as consumption increasingly diverges between higher- and lower-income households. With tenant demand remaining resilient, leasing conditions continue to be favorable. Shop occupancy is trending toward record highs, leasing spreads remain healthy, and contractual rent escalators continue to support low- to mid-single-digit same-store NOI growth.

While mall traffic and tenant sales remain healthy, Mall REITs still need to actively address legacy issues related to vacant anchor spaces. At Macerich, management is executing a large-scale leasing and redevelopment initiative called Path Forward, which involves repositioning roughly 25% of the portfolio through new tenants and anchor replacements. All 30 anchor spaces have now been committed, and management expects the improved tenant mix to strengthen renewal negotiations and support earnings growth as the targeted USD 140m signed-not-opened pipeline comes online through 2028.

In Canada, Hudson’s Bay, the last major department store anchor, filed for bankruptcy last year. This will temporarily pressure Primaris’ occupancy, leading to same-store NOI growth of only 1-2% in 2026, but also creates future leasing upside. Primaris sees attractive acquisition opportunities as pension funds reduce mall exposure, potentially creating a USD 40-50bn pool of assets. Primaris has been a net buyer since 2021 and faces limited competition for acquisitions.

Apartments

Apartment meetings, particularly with the Sunbelt REITs, were surprisingly positive from our perspective. For nearly three years, Sunbelt markets have struggled with an oversupply problem that drove heavy concessions, weak new lease growth, poor FFO/share growth, and prolonged stock underperformance.

Each time the outlook appeared to stabilize, new deliveries continued to hit the market while demand softened. The fear of slower white collar job growth, tied to corporate efforts to manage headcount and improve efficiency through AI, has also weighed on sentiment and is being reflected in lower share prices and implied cap rates in the above 6% range.

Concessions, the leading indicator for apartment fundamentals, are finally declining. This was a central theme for Mid America Apartments (MAA), both in meetings and in their conference materials. Concessions in MAA’s markets still average about two months of free rent (One month of free rent reduces effective rent growth on that unit by roughly 8.25%) but the trend is now moving steadily lower. If demand can hold steady, the combination of falling supply and declining concessions should tighten the market and support stronger new lease and renewal growth throughout 2026 and especially as we head into 2027.

In Atlanta, Independence Realty Trust (IRT) previously offered concessions on about 35% of leases at roughly $1,300/unit. That figure has already trended down toward 30% and $1,200, and management expects it to fall toward 25% and $1,000 as new supply is absorbed. Occupancy remains stable, and IRT expects rent growth to improve in the second half of the year as concessions burn off.

Despite these improving indicators, the market remains laser focused on job growth concerns and renter demand. However, a steady decline in concessions has historically marked the beginning of a recovery in effective rents, and the current setup suggests the narrative will shift from chronic apartment oversupply toward a focus of improving fundamentals as supply is successfully absorbed.

Office

Office was one of the most debated sectors at the conference. The dominant narrative is that AI will replace white-collar workers, reducing the jobs that drive office demand. That fear has created a sharp divergence in performance: office REITs are down 13.7% YTD, while the broader REIT index is up 8.2%. The selloff has been sharp despite the fact that the highest quality office REITs own Class A, trophy assets where occupancy remains higher than the market average.

Manhattan office REIT SL Green (SLG) is a clear example. SLG same store occupancy was 88% in Q4 2024, rose to 90.6% by Q4 2025, and we expect it to move above 93% this year. Manhattan is the tightest office market in the country and leasing activity is strong, with SLG already signing another 490k sf in early 2026. In Manhattan, SLG is seeing increased occupancy, positive rental growth, declining concessions, and lower use of free rent – all positive signs. These improving trends contrast sharply with the predictions made during Covid that Manhattan office was “dead” and that NYC workers would never return to high rise towers as they shifted to remote work.

| SLG – Manhattan Office Leasing Metrics | Q4 2024 | Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 |

|---|---|---|---|---|---|

| Occupancy | 88.0% | 88.6% | 89.2% | 90.9% | 90.6% |

| Starting cash rent psf | $80.72 | $84.80 | $79.27 | $95.42 | $84.32 |

| Previous cash rent psf | $71.18 | $88.34 | $88.68 | $90.77 | $83.28 |

| Change in new cash rent | 13.4% | (4.0%) | (10.6%) | 5.1% | 1.3% |

| Tenant Concessions psf | $102.30 | $109.37 | $111.53 | $108.39 | $46.69 |

| Average Lease Term | 10.5 | 9.1 | 10.1 | 10.5 | 5.7 |

| Free Months Rent | 11.8 | 9.5 | 11.4 | 9.1 | 4.2 |

Healthcare

The senior housing operating (SHOP) subsector continues to attract new entrants as investors recognize just how strong the supply and demand fundamentals have become. The demographic backdrop is exceptional, and leaders in the space such as Welltower (WELL) and Ventas (VTR) have shown how powerful earnings growth can be in a business where even modest occupancy gains drive meaningful operating leverage.

Smaller healthcare REITs and private buyers are trying to follow them into the space, but the advantage still sits with the largest platforms. WELL, VTR, and AHR have a clear cost of capital and first mover advantage, allowing them to buy the highest quality assets in the best submarkets and do so at scale. Even after WELL’s 232% total return over the last five years, new supply remains limited because construction costs are high, entitlement timelines are long, and the operating model is complex.

Across the sector, the message is consistent: demand is accelerating, supply is constrained, and the companies with scale, cost of capital advantages, and deep operator experience are best positioned to capture the opportunity. New smaller entrants will continue to appear, but the leaders are securing the highest quality assets and generating the strongest growth. We would be cautious about moving down the risk spectrum as smaller healthcare REITs try to build SHOP exposure, despite the hype amongst investors.

Asset Tour Pictures

Miami Property Tours (EGP, TRNO, FRT) – 1 & 4 March 2026

|  |

|  |

Download the PDF version of the report here